Former Federal Reserve Chairman Ben Bernanke used extraordinary tools to fight the financial crisis, and a decade later the Fed is having a hard time putting them away.

When Lehman Brothers failed 10 years ago, the Fed and other government agencies took all types of actions to head off a collapse of the financial system and to bolster the banking sector. Fed officials are still unwinding some of those moves, and chances are the hangover from those policies will be with them well into the future.

"It required a lot of creativity to come up with solutions that would stabilize the market and exist in the limit of the law," said Mark Cabana, head of U.S. short rate strategy at Bank of America Merrill Lynch. "The market is still dealing with a lot of these legacy issues today and it's taking a long time to undo some of the actions that were put in place during the financial crisis to ensure that a financial crisis like we had a decade ago doesn't happen again."

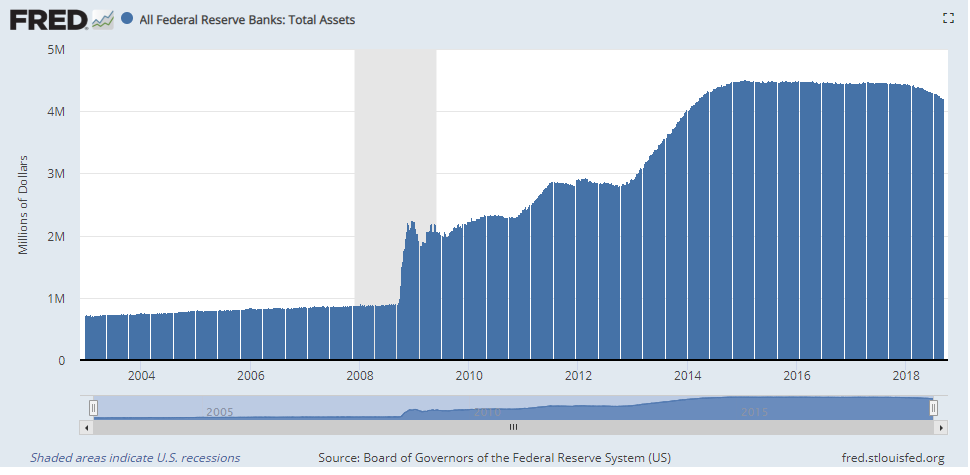

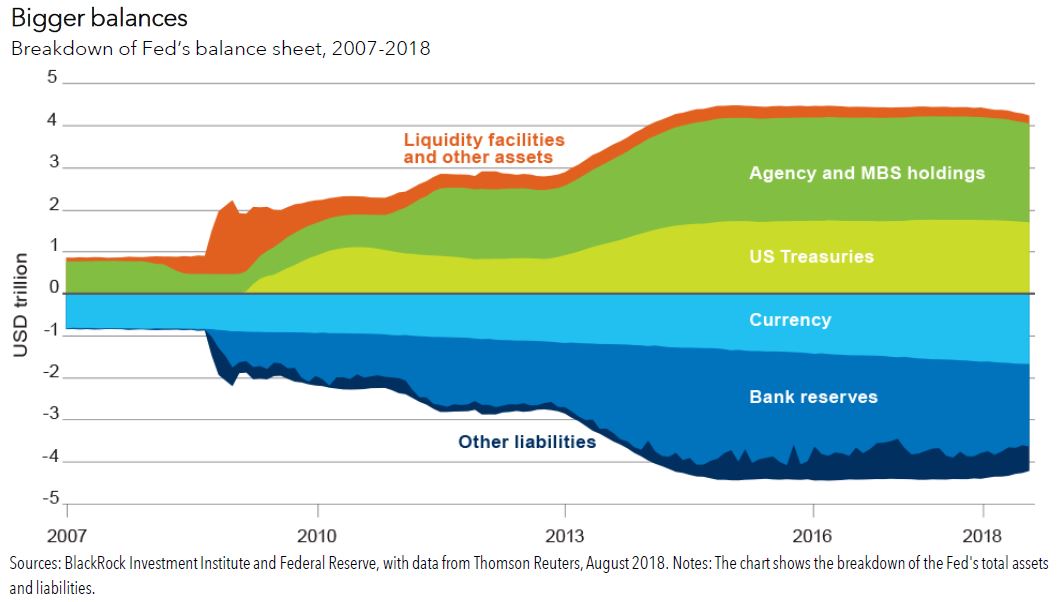

The Bernanke Fed used untested measures, such as pumping liquidity into the banking system, slashing interest rates to zero and buying Treasury and mortgage securities in a "quantitative easing" program that ballooned its balance sheet to a high of $4.5 trillion. In a post-crisis regulatory response, banks were reigned in, subjected to higher capital requirements and mandatory stress tests.

The Fed's balance sheet

Source: St. Louis Fed

Bernanke's successor, former Fed Chair Janet Yellen, made the first moves to "normalize" interest rates after the crisis. And now Fed Chairman Jerome Powell has been raising rates and chiseling away at the balance sheet with a program to "taper" back purchases of securities. The Fed had previously repurchased securities to replace all that were maturing, and now it only replaces some of them as they run off, shrinking its balance sheet as a result.

For consumers, the Fed's policy reversal means mortgage rates are rising, and other consumer loans are also more expensive. A 30-year fixed rate mortgage, now at about 4.6 percent, is well above the rate a year ago when it was less than 4 percent. Interest rate incentives, such as zero percent financing on autos, are also going away.

In the Treasury market, the 2-year note yield, which closely tracks Fed policy, was at 2.736 percent, the highest level since the summer before Lehman failed.

The slow pace of reversing these policies is part of an evolution of the major central banks, which have changed with their environment. The Fed's financial crisis policies have become part of its took kit.

"Central banks, led by the Fed saved the day, and really sort of prevented a repeat of the Great Depression, which is where we were," said Elga Bartsch, who heads economic and markets research at BlackRock Invesment Institute. "They clearly averted that. That doesn't mean we've completely sprung back to health."

Financial conditions are still supporting growth and financial markets, but "in the coming quarters the Federal Reserve will likely push interest rates closer to a neutral level," she said. Neutral is the level that neither stimulates or slows the economy, but it's precise number is a matter of debate.

Since the Federal Reserve began raising interest rates in December 2015, markets have been skeptical the Fed will actually follow through with its forecasts, since the Fed has backed away at signs of trouble for the economy and markets.

Futures markets still project low odds for more than one rate hike on the fed funds rate, while the Fed forecasts three. Reversing course from quantitative easing might create issues no one has foreseen.

"We just don't know over time if there's something that could tip the apple cart," said Diane Swonk, chief economist at Grant Thornton. "There's no way to predict or model what might hit the Fed….they're trying to make sure they communicate well what they're trying to do so nothing goes awry. We're in uncharted waters."

The Fed is expected to raise its fed funds target rate in late September and again in December. That would put it at 2.25 to 2.5 percent by the end of the year. But economists say the Fed may not get rates anywhere near what used to be viewed as a normal neutral rate before it stops hiking.

Swonk said the Fed could slow its tapering or even start buying debt again if it were to face a new crisis, but the effect may be minimal. The Fed could also drive rates back down to zero. "There's no easy answer on this one. There have been things put in the financial system to guard against the problems we've had, but that means we could get a crisis somewhere else that could hit in a different way. It's not hard to come up with a list of what could go wrong."

Fed officials, however, have been eager to raise rates, to both give themselves a cushion for any new crisis and to prevent unintended consequences of bubbles in the economy. The Fed has raised rates seven times since 2015 in an effort to get back to a more normal level.

Joseph LaVorgna, Natixis' chief economist for the Americas, is in the camp that believes the Fed could cause trouble for the economy if it hikes as much as it forecasts. He points to the signal coming from the difference between the short-term and longer term rates, which is narrowing, or flattening in bond market parlance. That is viewed as a possible warning about future economic growth, and Fed rate hiking could speed the flattening process.

If the so-called yield curve actually inverts, where the short end yield on a 2-year note, for instance, rises above the longer term 10-year note yield, that would be taken as a strong indication of a coming recession.

"The market is very sophisticated. It sniffs these things out before the Fed," he said. "Certainly, whenever the next equity correction comes, it could be large enough to thwart the Fed."

Some of the skepticism about future rate hikes has been because of low inflation, which has recently picked up and now meets the Fed's 2 percent target. Another reason is that there could be some event that affects the economy and slows the Fed, like a broader trade conflict or the emerging markets selloff, which some blame on the the central bank.

"The Fed is contributing to higher interest rates, more dollar strength. That complicates things for emerging markets, so the Fed is certainly contributing to some of the stress we're seeing in emerging markets," said Bank of America's Cabana. But that's only part of the story and if the Fed was the sole force behind the weakness in the emerging world, financial conditions would be tighter, he said.

BlackRock's Bartsch said the Fed may be having some influence but emerging markets are having their own issues. "They are first and foremost idiosyncratic stories."

Countries that have seen their currencies particularly hard hit, like Argentina and Turkey, have their own specific problems with inflation and high borrowing costs. Separately, Brazil, which also has been hit, is more at risk because of political uncertainty ahead of its upcoming election.

If the problem were the Fed, "you would expect the impact to be much more widespread and not just limited to emerging markets but also the credit complex in the U.S. and other risk assets," Bartsch said.

Bartsch said quantitative easing may not have been the booster to risk assets that many thought it was. But it may have helped the Fed communicate that it would keep rates low, because as long as it was buying assets, it was not raising rates. Bartsch said the wind down is much more telegraphed to the market than the start of easing, which was expected to affect financial markets.

Now there are doubts the Fed will be able to continue scaling back its balance sheet as much as previously thought. Powell has said the Fed this fall will review the balance sheet, which is still at about $4.2 billion.

"I would not expect to hear any policy action on the balance sheet wind down just yet but more the framework on how they think about it," said Bartsch.

In part due to new rules for bank capital, banks are keeping much more of their cash at the Fed than they used to. This has resulted in a higher interest rate on excess reserves, and has driven that rate closer to the fed funds rate, the short-term rate the Fed influences with its target range.

"There are no transaction costs associated with it. Right now, they receive a relatively attractive rate of return versus other alternatives, and I think they see this as the cleanest means with which they can meet their regulatory guidance," said Cabana.

The interest on excess reserves, or [IOER] is now 3 basis points above the fed funds rate, compared to an average spread over the past five years of 12 basis points, Cabana said.

Strategists said the Fed will likely decide on what to do about its balance sheet program sometime next year.

Bartsch said concerns about the Fed's policy unwinding are overblown and that the market shouldn't see it as merely the reversal of quantitative easing.

"It is a very different context in which it happens," she said. "Back when quantitative easing started, we had severe balance sheet stress in many private financial institutions...The Fed's balance sheet was the only one growing that was able to grow in a meaningful way."

Bartsch said the tools the Fed has used for the crisis will not go away, and they could be used in the future if needed.

"This was a once in a generation financial crisis., and a once in a generation global recession," she said. "Very specific situations created in the process takes some time..I know that people talk about central bank normalization.... if it was normal, why did we have the financial crisis?"

via IFTTT

No comments:

Post a Comment